TSLA made $100MM in 1 month of trading crypto, more than it ever made selling cars in 14 years (ex reg credits). It should shut all money losing ventures and become a full time trading desk.

Wall

Street expectations from TSLA's earnings today are rather stratospheric,

but as Bloomberg notes, even if the company misses big, the S&P 500

likely won’t be in the doldrums tomorrow because of it. Why? Simply

put, the electric-vehicle maker matters less than other high-profile

stocks in the broad market gauge.

Alphabet, Amazon.com, Apple,

Microsoft and Tesla are among the most influential companies in the

stock market. But by one simple measure, Tesla looks different than the

others. The S&P 500’s 30-day positive correlation with the stock has fallen to ~0.44 from an early March peak of almost 0.8. That

pales in comparison with Microsoft at ~0.77, Apple at ~0.72, Amazon at

~0.68 and Alphabet at ~0.65. In fact, the S&P 500’s correlation with

old-school cyclical Caterpillar -- which also reports this week -- is

higher than Tesla at ~0.51. This falling correlation is inevitable

as Tesla has gained less than 5% this year compared with over 11% for

the S&P 500, with value sectors such as energy and financials

outperforming. This has happened as meme stocks like GameStop have

pushed Tesla out of the limelight, while Bitcoin has attracted almost

all the buzz.

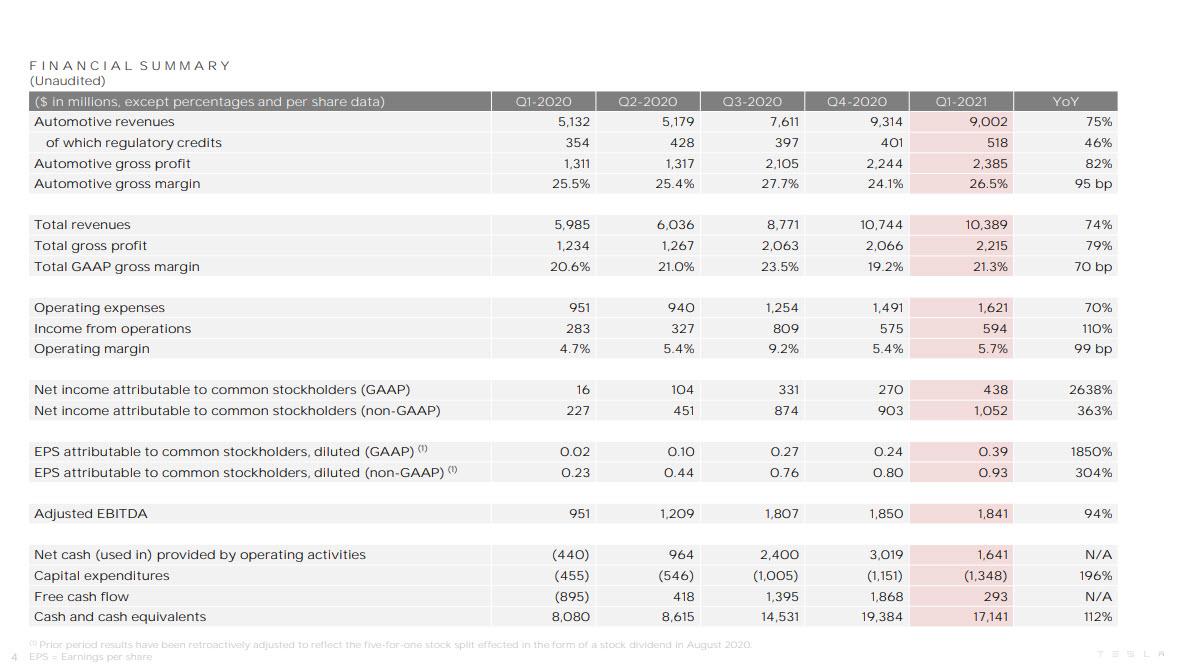

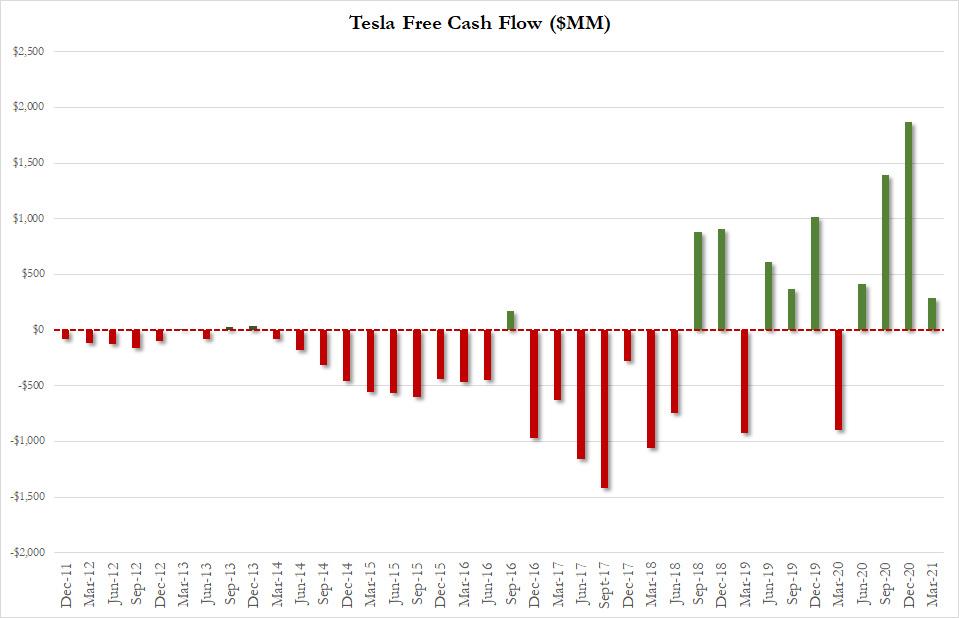

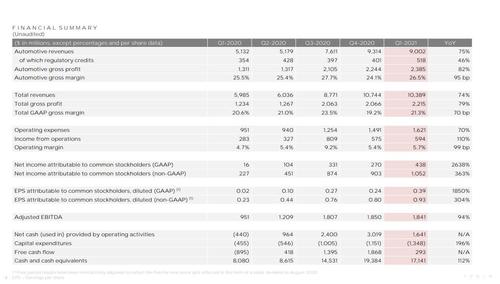

With that in mind, here is what TSLA reported shortly after the close for Q1:

- Adjusted EPS of 93C, beating est. 80c

- Revenue $10.389BN, missing est. $10.42 billion (range $8.20 billion to $12.34 billion)

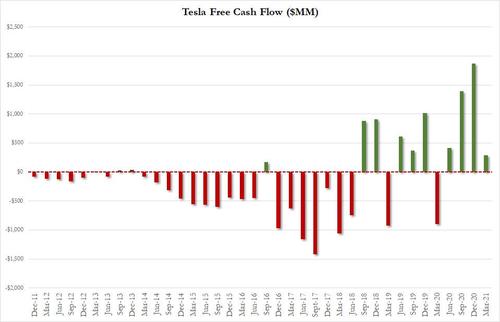

- Free Cash Flow $293MM, beating est. of cash burn of $82.8 million

- Automotive gross margin +26.5%, beating est +24.3%

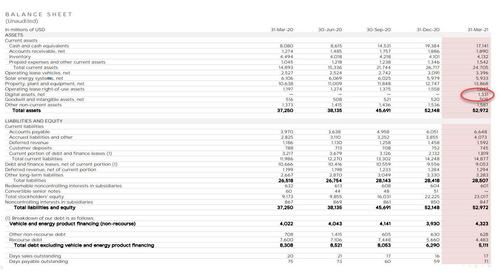

- Cash and cash equivalents $17.14 billion, missing estimates of $17.90 billion

The results visually:

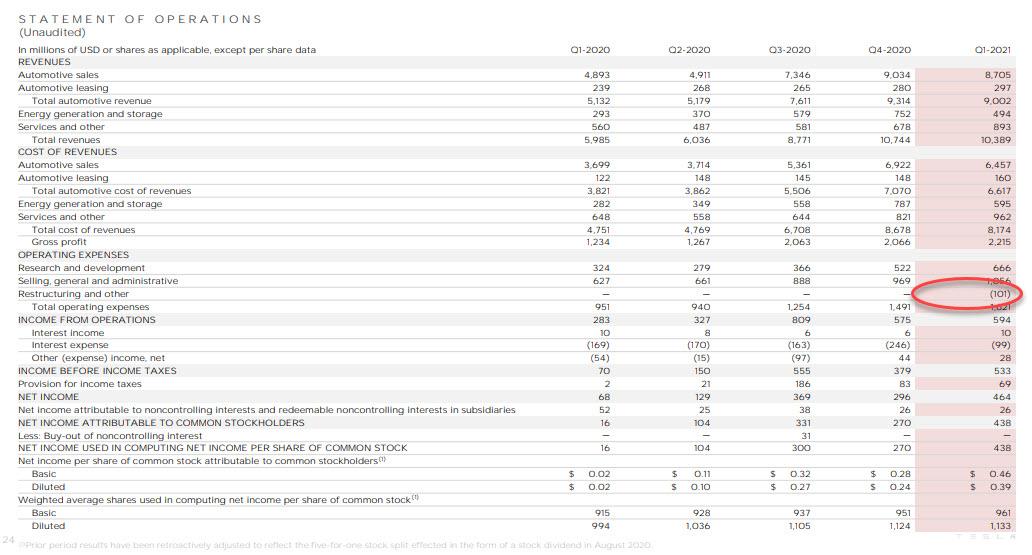

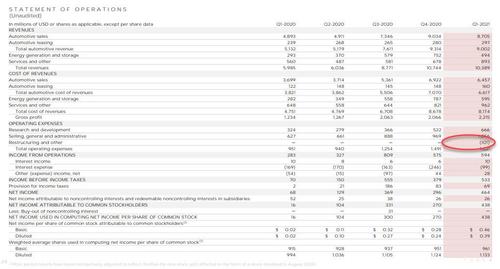

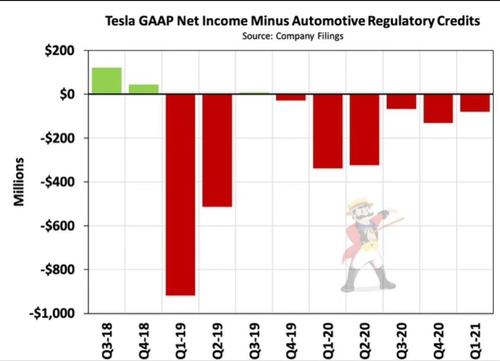

But here is the problem: TSLA

reported $594MM in income from operations, but regulatory credits

accounted for a whopping $518MM of it, the highest on record and up from

$401MM in Q4 2020.

So

while GAAP net income was just $438MM, this means that for yet another

quarter the company did not generate actual net income without

regulatory credits. Add that another $101MM in profits came from "sale

of bitcoin"...

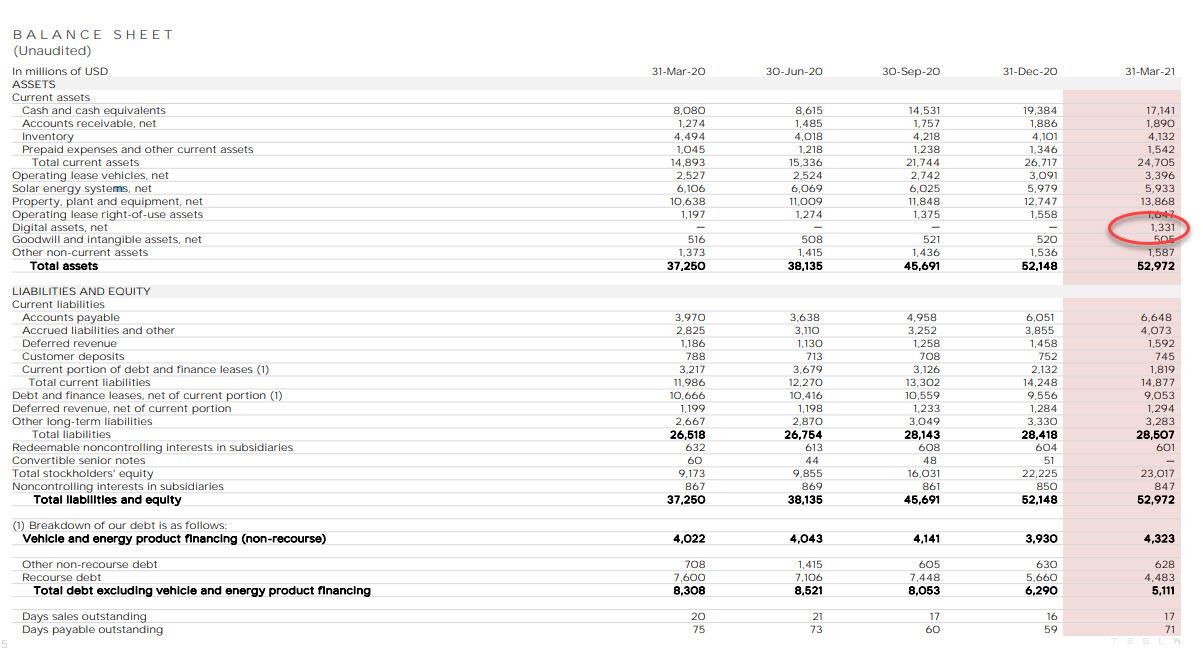

...

with TSLA owning $1.3BN in digital assets at the end of the quarter,

which means it sold around $272MM of the bitcoin it previously owned.

So in addition to over half a billion in reg credit sales, made $101MM in profits from sale of $272MM in bitcoin (reducing its total from $1.5BN to $1.331BN at the end of the quarter).

And while everyone assumes that this is all bitcoin, it is unclear how much of TSLA's "digital assets, net" was Dogecoin.

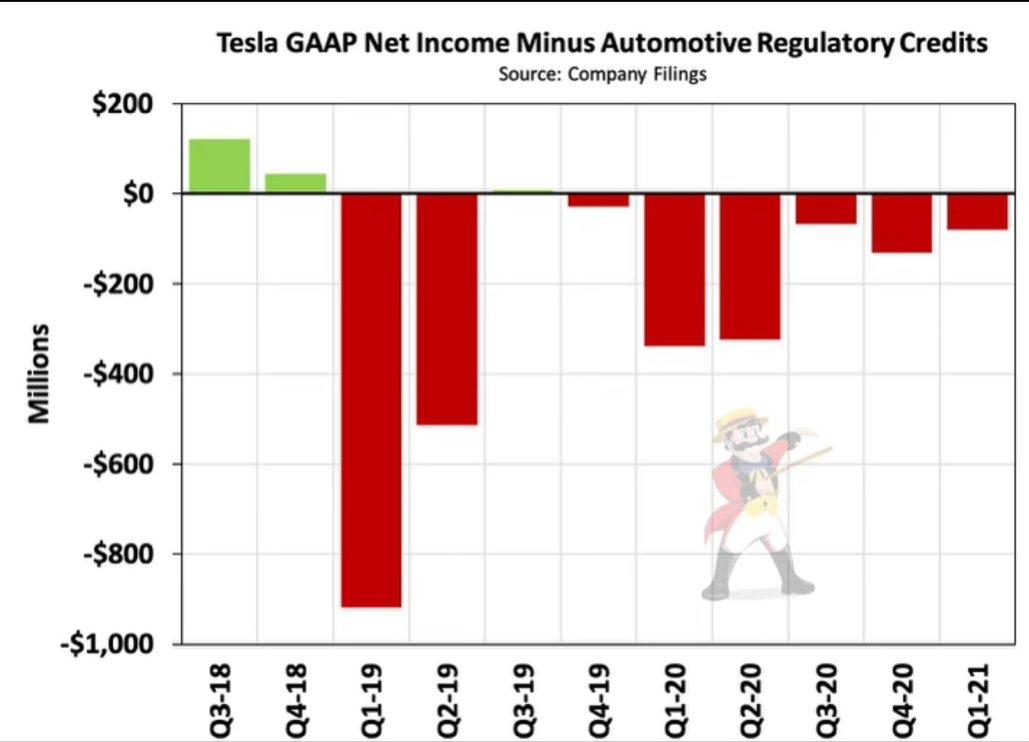

Of

course, some will claim that non of this matters, and that TSLA has in

fact generated 7 consecutive quarters of profits, although if one strips

reg credits from the GAAP Net Income, this is what one gets.

Discussing

its profitability, TSLA said that its operating income improved in Q1

compared to the same period last year to $594M, resulting in a 5.7%

operating margin. "This profit level was reached while incurring SBC

expense attributable to the 2018 CEO award of $299M in Q1, driven by an

increase in market capitalization and a new operational milestone

becoming probable."

On a year over year basis, Tesla said

that positive impacts from volume growth, regulatory credit revenue

growth, gross margin improvement driven by further produt cost

reducstions and sale of bitcoin were mainly offset by a lower ASP,

increased SBC, additional supply chain costs, R&D investments and

other items. Model S and Model X changeover costs negatively impacted

both gross profit as well as R&D expenses.

In terms of

Tesla’s financial performance, it’s a case of better-than-expected

Automotive Margins and free-cash-flow. The company said of its profit

outlook: "We expect our operating margin will continue to grow over

time, continuing to reach industry-leading levels with capacity

expansion and localization plans underway."

The company also

disclosed that it is on track to start production from Berlin factory in

2021, adding that first deliveries of the new model S should start

shortly.

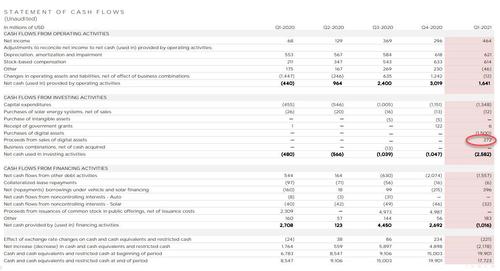

On the cash flow side, TSLA revealed that it had a $1.2BN

net cash outflow related to bitcoin in Q1, as well as net debt

repayments of $1.2BN offset by free cash flow of $293MM, which was above

the estimate of $83MM in cash burn:

Quarter-end cash

and cash equivalents decreased to $17.1B in Q1, driven mainly by a net

cash outflow of $1.2B in cryptocurrency (Bitcoin) purchases, net debt

and finance lease repayments of $1.2B, partially offset by free cash

flow of $293M

Looking

ahead, Tesla said it expects to achieve 50% average annual growth in

vehicle deliveries over a multi-year horizon. But the company notes that

rate of growth will depend on equipment capacity, operational

efficiency and capacity and stability of supply chain.

Tesla’s timeline also remains largely intact. From the shareholder letter:

“We

are currently building Model Y capacity at Gigafactory Berlin and

Gigafactory Texas and remain on track to start production and deliveries

from each location in 2021. Gigafactory Shanghai will continue to

expand further over time. Tesla Semi deliveries will also begin in

2021.”

Something else the market may not like is

that the average selling point for a Tesla fell 13% in the first

quarter. According to the company, this is "because Model S and Model X

deliveries reduced in Q1 due to the product updates and as lower ASP

China-made vehicles became a larger percentage of our mix."

Elsewhere,

there was no substantive mention of Cybertruck anywhere in the

shareholder presentation, just that it’s a product ‘in development’

listed under the Texas plant. As Bloomberg reminds us, "Musk has said on

prior calls that small volumes of Cybertruck deliveries could be

possible by the end of this year. Will he give an update on that during

the earnings call?"

Not surprisingly, not even TSLA's usual

cheerleaders were ecstatic about the results: “Everything happened that

people thought would happen,” Munster told Bloomberg. “There’s not a lot of news and it wasn’t a blowout.”

* * *

In

kneejerk response to the earnings, Tesla shares were first up, but then

slide more than 1% in postmarket, which nonetheless was a much tamer

reaction than what options trading was pricing in ahead of the results.