New Delhi, Jan 25 : The Confederation of All India Traders (CAIT) in a

communication sent to Union Commerce Minister Piyush Goyal demanded

immediate action against e-commerce entities including Amazon, Flipkart,

Zomato, Swiggy and others."It is a case of daylight robbery of

e-commerce entities in India and therefore demand immediate action

against the erring e-commerce portals and online mechanism providers,"

CAIT said.

CAIT has accused Amazon, Flipkart, Zomato, Swiggy and various other

e-commerce entities for violation of mandatory display of Country of

Origin and Manufacturer, seller Details on products sold through their

respective E-Commerce Portals as required under the Consumers Protection

(E Commerce) Rules,2020, Legal Metrology (Packaged Commodities) Act,

2011 and guidelines of Food Safety & Standards Authority of India.

CAIT has asked Goyal to take action against E-commerce entities including Amazon, Flipkart, Zomato, Swiggy and others.

"It is a case of daylight robbery of e-commerce entities in India

and, therefore demands immediate action against the erring e-commerce

portals and online mechanism providers," CAIT said.

CAIT National President B.C. Bhartia and Secretary General Praveen

Khandelwal in a communication to Goyal said that e-commerce entities

conducting business in India including Amazon, Flipkart and others are

highly violating the mandatory conditions spelled out in above Acts.

"It

is a pity that particularly in e-commerce every guidelines, Rules &

Regulations, Laws and policies are being flouted openly and no

department has so far taken any cognizance of compliance issues

resulting in a highly vitiated and mess like e-commerce trade of India,"

CAIT said.

Bhartia and Khandelwal said that Rule 10 of Legal Metrology

(Packaged Commodities) Rules, 2011 provide that e-commerce entities

should have to display name and address of the manufacturer, name of the

country of origin, common/generic name of the product, net quantity,

best before/use by date (if applicable), maximum retail price,

dimensions of the commodity, etc.

This rule was introduced in June 2017 and provided a transition

period of six months thereby its implementation from January 1,2018 but

even after a lapse of three years, the above rules are not being

complied by e-commerce companies prominently by Amazon, Flipkart, etc.

Advertisement

Failure

to make declarations as above will amount to selling non-standard

packages and will invite penalty under the above said Act, including

fine or imprisonment or both, CAIT said.

Both trade leaders further said that similar obligations were

imposed on e-commerce food business operators vide guidelines issued by

the Food Safety & Standards Authority (FSSAI) on February 2,2017.

"But such FBOs like Zomato, Swiggy, etc. are not complying with the above rules," CAIT said.

Advertisement

Bhartia

and Khandelwal said that under Rule 4(2) of the Consumer Protection (E

Commerce) Rules, 2020, it is provided that every e-commerce entity shall

provide the following information in a clear and accessible manner on

its platform, displayed prominently to its users, namely, legal name of

the e-commerce entity, principal geographic address of its headquarters

and all branches, name and details of its website, and contact details

like email address, fax, landline and mobile numbers of customer care as

well as of grievance office. Similar provisions are also spelled out in

Press Note 2 of the FDI Policy, 2016.

CAIT said no e-commerce entity has appointed a Nodal Officer as also

complying with above provisions. Important rights of the consumers are

being violated as they are not aware of the seller or description of the

product at the time of purchase of products from e-commerce portals.

A 3,600-page supplementary

chargesheet, filed by Mumbai Police on January 11 in the TRP scam case,

includes a BARC forensic audit report, WhatsApp chats purportedly

between Partho Dasgupta and Arnab Goswami, and statements of 59 persons,

including former council employees and cable operators.

By Mohamed Thaver

, Krishn Kaushik Partha Dasgupta and Arnab Goswami. (File Photo)

Mumbai, New Delhi, Jan 25, 21: The

former CEO of Broadcast Audience Research Council (BARC) India, Partho

Dasgupta, has claimed in a handwritten statement to Mumbai Police that

he received US$12,000 from Republic TV Editor-in-Chief Arnab Goswami for

two separate holidays and a total of Rs 40 lakh over three years, in

return for manipulating ratings in favour of the news channel, according

to the supplementary chargesheet filed in the TRP scam case.

The 3,600-page supplementary chargesheet, filed by Mumbai Police on January 11, also includes a BARC forensic audit report, WhatsApp chats purportedly between Dasgupta and Goswami, and statements of 59 persons, including former council employees and cable operators.

The

audit report names several news channels, including Republic, Times Now

and Aaj Tak, and lists instances of alleged manipulation as well as

“pre-fixing” of ratings for the channels by BARC’s top executives.

The

supplementary chargesheet was filed against Dasgupta, former BARC COO

Romil Ramgarhia and Republic Media Network CEO Vikas Khanchandani. A

first chargesheet was filed against 12 persons in November 2020.

According

to the second chargesheet, Dasgupta’s statement was recorded in the

office of the Crime Intelligence Unit on December 27, 2020, at 5.15 pm,

in the presence of two witnesses.

Dasgupta’s

statement reads: “I have known Arnab Goswami since 2004. We used to

work together in Times Now. I joined BARC as CEO in 2013. Arnab Goswami

launched Republic in 2017. Even before launching Republic TV he would

talk to me about plans for the launch and indirectly hint at helping him

to get good ratings to his channel. Goswami knew very well that I know

how the TRP system works. He also alluded to helping me out in the

future.”

It

states: “I worked with my team to ensure manipulation of TRP ratings

that made Republic TV get number 1 rating. This would have continued

from 2017 to 2019. Towards this, in 2017 Arnab Goswami had personally

met me at St Regis hotel, Lower Parel and given me 6000 dollars cash for

my France and Switzerland family trip…also in 2019 Arnab Goswami had

personally met me at St Regis and given me 6000 dollars for my Sweden

and Denmark family trip. Also in 2017, Goswami had personally met me at

ITC Parel hotel and given me Rs 20 lakh cash… also in 2018 and 2019…

Goswami met me at ITC hotel Parel and gave me Rs 10 lakhs each time…”

Dasgupta’s

lawyer Arjun Singh said: “We totally deny this allegation as the

statement would have been recorded under duress. It does not have any

evidentiary value in the court of law.” When contacted, a member of

Goswami’s legal team declined to comment. Goswami has repeatedly denied

any wrongdoing and alleged he was being targeted.

The

chargesheet also includes BARC’s audit report, dated July 24, 2020,

which states that evidence “indicated favouritism shown to few channels”

and “in some cases, we suspect that the ratings were pre-decided”.

For

instance, the report mentions alleged suppression of viewership for

Times Now to boost Republic’s weekly rankings, and highlights a

purported conversation between BARC’s top executives and a senior

marketing executive of India Today Group on “pre-fixing” Aaj Tak’s

ratings.

With multiple emails and messages between BARC officials

attached as annexures, the report states that one of the reasons given

by the council for changing Times Now’s viewership data is to cater for

“outlier” data, which is meant to identify spikes in viewership due to

the channel being the “landing page” on some distributors.

The

practice of placing a channel on the “landing page” was prohibited by

the Telecom Regulatory Authority of India. But that direction was set

aside by the Telecom Disputes Settlement and Appellate Tribunal, and the

matter is now in Supreme Court.

The audit was conducted by

Acquisory Risk Consulting. The executive summary of the audit report

states that “manipulation was evidenced in 2017, 18 and 19 across

English News Genre and Telugu News Genre”.

The report states that

six top executives of BARC at the time were involved in “manipulation of

ratings and violation of the code of ethics” between 2018 and 2019,

including Dasgupta, Ramgarhia, Head of Products (South) Venkat Sujit

Samrat, Head of West Rushab Mehta, Vice President of Strategy Pekham

Basu, and Chief People Officer and Strategy Manashi Kumar.

In

October 2019, Dasgupta was replaced by Sunil Lulla as CEO. The

supplementary chargesheet includes a statement by a BARC official

claiming that in “February 2020, Sunil Lulla told me that there were

allegations of TRP rating manipulation from the media industry” against

Dasgupta, Ramgarhia, Mehta, Samrat, Kumar and AVP Pekham Basu. The

official states that in “the first week of June 2020, from the server I

took the backup of the emails of the suspected persons on a hard drive

and gave Ramgarhia’s laptop in the last week of June” to the auditing

agency.

Mehta, Samrat, Kumar and Basu have not been charged by

police. The audit report was provided to Mumbai Police in December, two

months after it registered an FIR in the TRP case.

Some of the

instances cited in the report point to changed ratings that resulted in

Republic being the top channel in English news from 2017. It cites

emails and messages as evidence for weeks in which Times Now’s data and

ratings were decreased, giving Republic the edge.

On June 18,

2017, the report states, Mehta wrote to Ramgarhia: “As required, Times

Now numbers are changed, while Republic is kept the same”. According to

the report, “this is pointing that the senior management wanted Republic

TV to be number 1, and the team was working to achieve this objective”.

According

to the audit report, conversations between BARC’s executives and a top

marketing executive of India Today Group, in 2016, pointed towards

“pre-fixing” the ratings for Aaj Tak. The report cites “chat message

conversations between Romil, Partho, and external officials of channels,

hinting about pre-fixing the channel ratings during our analysis”.

When

contacted, BARC said in an email: “As the matter is a subject of an

ongoing investigation by the various law enforcement agencies, we are

constrained to respond to your enquiries.”

Republic said in a

statement that “there has been a collusion of corporate and political

interests to target” Goswami. “This collusion, which is a result of

commercial, political and personal interests, is aimed, quite obviously,

at illegally trying to create prejudice against the Republic Media

Network,” it said.

Times Now defended the use of landing pages,

stating that they are “not ruled as illegal” and “are simply the most

preferred frequency which is sold and bought at a Premium by perfectly

legal means”. It said the outlier policy was “abused by corrupt BARC

officials to manually intervene and wilfully and deliberately improve

channel ranks for favoured channels” and that it is “contemplating legal

action”.

India Today Group did not respond to queries from The Indian Express.

While

Dasgupta is in jail, The Indian Express reached out to Mehta, Samrat,

Ramgarhia, Kumar and Basu. Only Kumar responded. “I had remotely nothing

to do with research or ratings as it was a different team which handled

market analytics and data,” he said, adding that everything else was

“slander”.

The chargesheet also includes statements by cable

operators that they were asked to show Republic on two channels to

increase its TRP in exchange for money — two operators said they were

asked to raise vouchers of Rs 11,800 each.

FULL STATEMENT FROM TIMES NOW

“Times

Network uses only bonafide and legally valid means to do its business.

We do not indulge in Panel-Tampering or bribing BARC officials which are

common cheating practises followed by unscrupulous actors. TRP numbers

are a function of 2 factors: Reach of channel and Time Spent by Viewer

on the Channel (TSV). TSV depends upon the Content plan, style and

quality of story-telling. Reach depends upon Distribution efficiency and

Opportunity To See (OTS). There are laws of the land that govern

distribution, and as per them Landing Pages are not ruled as illegal.

Landing Pages are simply the most preferred frequency which is sold and

bought at a Premium by perfectly legal means. It is the same as FMCG

Companies strategy of acquiring best Shelf Space in supermarkets for

higher visibility. Or advertisers placing ads on the front page of

newspapers for highest visibility. This is available to all and is not

done by any underhand deals. Times Network has optimised its Product,

Brand and Distribution with the best in class inputs including Landing

Pages at high cost to deliver its channels to maximum viewers. It is

also worthy to note that such viewers are real and genuine as far as

advertising reach is concerned and the Advertiser gets the viewership

that he has paid for.

“The Outlier Policy of BARC to filter

Landing Pages is a contentious issue as this is not Spurious reach. It

is pertinent to note that the Landing Page Filtration Algorithm has been

officially announced by BARC only on Sept 03, 2020 after which Times

Network has challenged this in the Bombay High Court and the matter is

sub judice as on date. The 44 week Forensic audit is for the period May

2017 to March 2018 when no such Outlier Policy was in place and BARC had

no mandate to remove bonafide reach from landing pages. The outlier

policy or moderation policy is a mechanism provided by BARC Technical

Committee to remove statistically significant anomalies, mainly abnormal

TSV from unlikely homes or spikes in data that don’t represent the

logical true picture. The Outlier Policy is the key provision that has

been abused by corrupt BARC officials to manually intervene and wilfully

and deliberately improve channel ranks for favoured channels.

“Times

Network views this as the gravest breach of trust by BARC and is

contemplating legal action. The timing of misrepresentation of numbers

makes it even more damaging as it was done at a critical juncture in our

Brand history when Times NOW was engaged in a marketing battle,

energetically defending and retaining its position. The resultant

financial and brand impacts are being ascertained at the moment.”

Source: Indian Express

NEW

DELHI: Remote voting, or allowing a voter to cast her franchise from

any polling station in the country and not just the polling station or

constituency where she is registered, is among the key future

initiatives that the Election Commission is working on, chief election

commissioner Sunil Arora said on Sunday and added that mock trials of

the project would begin soon.

Sharing an “important dimension of the vision of Election Commission of India for future electoral processes”, Aro ..

Different

views have been delivered on this subject. It is the younger generation

that is buying bitcoin compared to who buys gold. On the other hand,

since the second half of 2020, more institutions have become buyers of

bitcoin. As JPM points out;

"...private gold wealth is mostly

stored via gold bars and coins the stock of which, excluding those held

by central banks, amounts to 42,600 tonnes or $2.7tr including gold

ETFs. Mechanically, the market cap of bitcoin at $600bn currently would

have to rise by almost x4.5 from here, implying a theoretical bitcoin

price of $146k, to match the total private sector investment in gold via

ETFs or bars and coins."

Source; JPM

This

is just a theoretical exercise. Before serious investments in bitcoin

could occur, volatility would need to converge and trade at similar

levels to gold volatility. Fund managers need to allocate money

according to volatility of each asset. Bitcoin vol converging to gold

volatility seems rather distant as of writing.

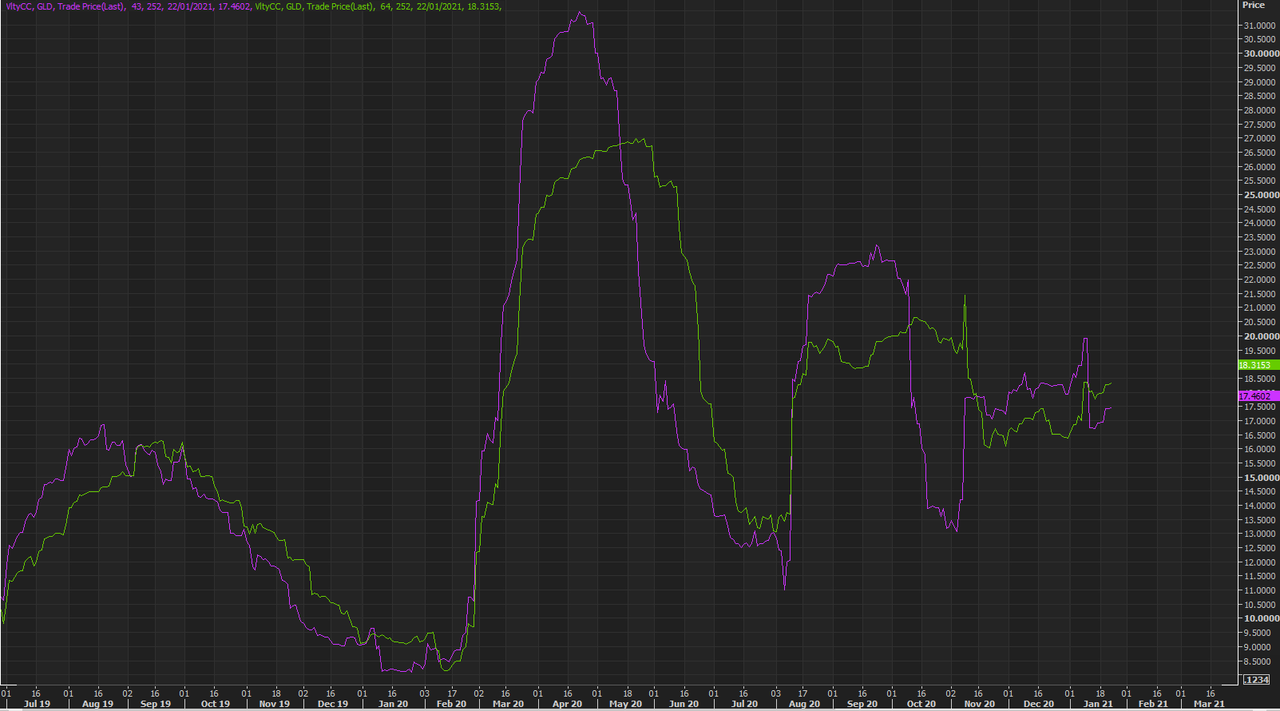

On the other hand,

average of bitcoin 1-2 mth bitcoin vol is around 85%. GLD 1-2 mth

average vol stands around 18%. That is aprox 4.7x higher vol for bitcoin

than gold. Apply the 4.7x to bitcoin's $600bn market and we have a "vol

adjusted" market cap of bitcoin matching gold. This is why we at TME

have been coming back to the argument explaining that most people have

no clue of how to manage downside volatility, and we see this as the

biggest "risk" for "non dynamic bitcoin fans".

So while many are arguing bitcoin is the new gold going forward, you could argue it is already here.

Source; Refinitiv

It

is easy to get carried away by a narrative that has worked, you made

money and lately your p/l diminishes, but you still trade the old

narrative. This has partly become the case with bitcoin lately. Same

arguments are made, but the price has been all but rosy.

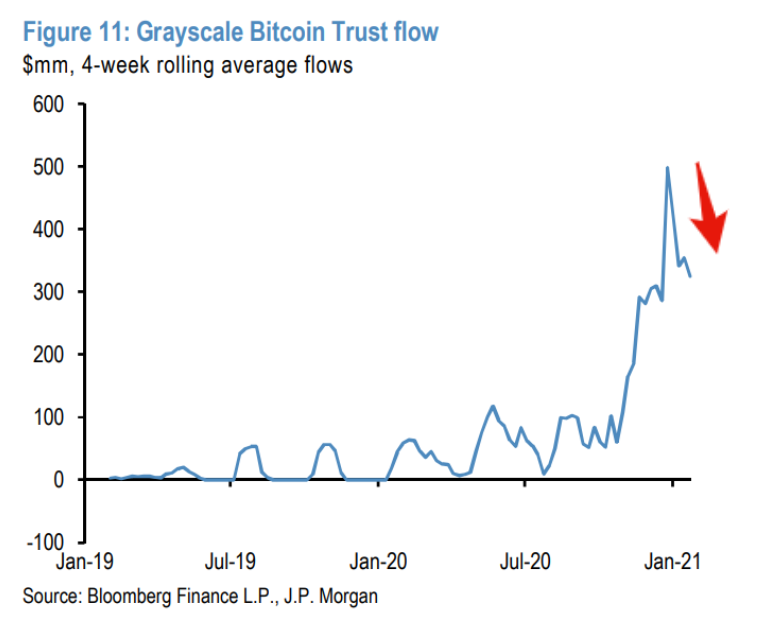

Institutional

buying sure, but let's not forget, institutions also have to manage

risk, so the new hot buys at 42k by some "smart" guys will need to be

sold when bitcoin falls. Grayscale bitcoin trust flow has been declining

lately...

Source; JPM

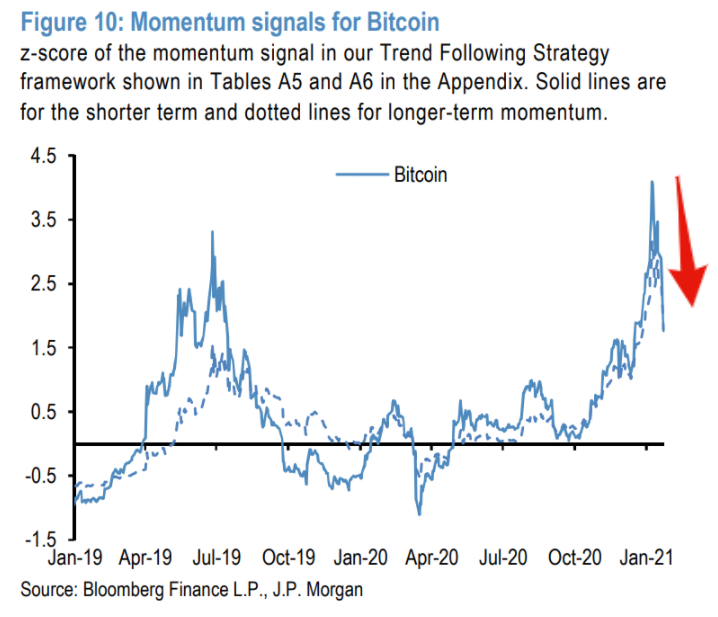

With

regards to momentum strategies that were pressing momentum higher,

especially during the illiquid Xmas and New Year weekends we outlined

weeks ago, they have no directional preference or bias.

Momentum

traders do not care about no blockchain nor fundamentals. They chase

momentum and have no emotions. Lately these momentum models are all but

pointing higher...

Source; JPM

What

about the short term px action? TME has been pointing out "why not try

the 50 day moving average" over past weeks (note Fibonacci 38.2% level

trades around that level as well). It would would be a first real

support to see how well new smart bulls have managed downside

exposure...

Is gold money? Many would say so, and a web search

returns tens of thousands of additional affirmative responses. If you

want to start a fight with a gold bug, take the opposite view.

But is it so?

To answer the question of whether gold is money requires a definition. This one, from Wikipedia, is typical:

Money

is anything that is generally accepted in payment for goods and

services and in repayment of debts. The main uses of money are as a

medium of exchange, a unit of account, and a store of value.

Wikipedia

refers to three properties of money. However, according to the Austrian

economist Carl Menger, its acceptability in trade is the defining

property. While money undoubtedly does serve as a store of value and a

unit of account, these properties are derivative, not definitional

properties. The reason that a medium of exchange necessarily is also a

store of value is the anticipation of its exchange value in the future.

[I]t

appears to me to be just as certain that the functions of being a

"measure of value" and a "store of value" must not be attributed to

money as such, since these functions are of a merely accidental nature

and are not an essential part of the concept of money.

Using the above definition, the question of whether any particular good is or is not money, can be posed in this way: is the good in question accepted as the final means of payment for transactions?

At present, in the developed world, nearly every nation has its own money or belongs to a currency union, such as the EU. Some nations in the developing world use the US dollar.

In highly inflationary environments, the local currency is often

spontaneously rejected in favor of the dollar or another foreign

currency. Hardly anywhere do we find gold generally accepted as a means

of payment. So gold must fail the definitional test of moneyness.

Is

this the end of the argument (and so the end of a very short article)?

Not quite. Gold is not money, but it has most of the desirable

properties of money, and the process by which it became money in the

past gives some clues about how it may become money once again.

A store of value is not necessarily a medium of exchange. As Menger says, a nonmonetary commodity can serve as a store of value:

But

the notion that attributes to money as such the function of also

transferring "values" from the present into the future must be

designated as erroneous. Although metallic money, because of its

durability and low cost of preservation, is doubtless suitable for this

purpose also, it is nevertheless clear that other commodities are still

better suited for it.

Analyst Paul van Eeden has

shown that gold has maintained its purchasing power relative to the time

that the gold standard ended. In "Is Gold an Inflation Hedge?" I

have provided links to Van Eeden's articles and a more detailed

discussion. I will summarize his analysis here. A theoretical gold price

equivalent which would give gold the same purchasing power as it had at

the end of the gold standard is calculated by taking the convertibility

ratio of $35 in 1933, and then multiplying by a factor representing the

growth in the quantity of fiat money from that time. Under the

classical gold standard, gold was the entire world's money. By counting

worldwide growth in currency (not only US dollars) and comparing it to a

worldwide price currency index of the gold price, van Eeden avoids the

pitfalls of looking only at gold's dollar price, which can experience

significant volatility due to the dollar's exchange rate against other

national currencies.

Van Eeden's research shows that,

since the end of the gold standard, the price of gold in units of fiat

currency has tracked its purchasing-power-equivalent price fairly well,

oscillating in a band around its theoretical value. In essence,

the purchasing power of gold has been reasonably stable in the time

since the end of the gold standard, which is only another way of saying

that gold has served as a store of value.

Even today most of the demand for gold is not for direct use, but demand to hold.

In the developed world, people purchase coins and bars for storage in

vaults. In other areas, people save by accumulating bullion jewelry.

Distinct from ornamental jewelry, bullion jewelry has low workmanship

value added. Its price is not much greater than the melt value of its

metal content.

The World Gold Council estimates that 52% of gold is held as jewelry.

James Turk subdivides jewelry holdings into low carat and high carat.

The former is purchased mainly for the gold value, as an alternative to

buying bars and coins. The latter is purchased mostly for fashion.

According to Turk's estimate (which

was published in 1996), monetary jewelry at that time accounted for

about 60% of jewelry with fashion jewelry accounting for the remaining

40%. However, even when made into jewelry, the gold is not destroyed and

can come back into the market as scrap. The WGC figures show

significant recovery from scrap.

That gold continued to be a store of value post–gold standard was unexpected by many economists. In the early 1970s, when the dollar's link to gold was cut, economist Milton Friedman predicted that the price of gold would collapse.4 The

Nobel laureate believed that the gold derived its value from its

relationship with the dollar; without gold backing, there would be far

less demand for gold. There would, of course, continue to be industrial

demand for the metal, but without monetary demand provided by the

dollar, the vast supply that had been accumulated during the preceding

centuries would overhand the market, depressing the gold price for the

foreseeable future. Friedman could not have been more wrong. It was the

dollar that collapsed in the 1970s, while the gold price in dollars

began a bull run that was not eclipsed in nominal terms until late last

year.

A similar and still widely held view in the world of mainstream financial analysts is that gold has been "demonetized." The

argument goes like this: central banks decide what money is; central

banks have determined that gold is not money; therefore gold is not

money. Only the stupid gold investors haven't figured this out. This

view of the gold market sees the price of gold as determined primarily

by central banks (who own an estimated 10–17% of aboveground supply).

The critical variable is how they will time the sales of their gold

hoards without causing a selling panic as market participants

realize that their gold coins and bars have no monetary value.

But why is gold a better store of value than most any of a vast number other nonmonetary goods? Why were Milton Friedman and

the other economists wrong? Their error was the assumption that

political institutions have the final say over what is and is not money.

But this is not so: the market has final say. Looking at the process by

which money originated from barter helps to understand why. According

to Menger, money came into being through the efforts of individuals to

expand the range of goods they could acquire through exchange beyond the

possibilities available. Some individuals in a barter economy begin by

bartering their goods for a commodity that they do not need but is

generally in demand throughout the market, with the intention of later exchanging that commodity for other goods. This strategy is called indirect exchange.

These astute traders realize that "the acquisition by trade of the

consumption goods that he needs…can proceed…much more quickly, more

economically, and with a greatly enhanced probability of success."

As

societies moved from barter to monetary economies, different goods were

in competition with each other for use as money. Over time, as monetary

exchange expanded in proportion to barter, some commodities were found

to work better as money than others, until only a handful of them became

"acceptable to everyone in trade." Those were gold and silver.

What qualities have made gold (and silver) the winners of the monetary competition in centuries past?

The qualities most often cited by monetary historians are durability,

divisibility, recognizability, portability, scarcity (the difficulty of

producing more of it), and a value-to-weight ratio that is neither too

high nor too low. Too low a ratio would make it hard to carry enough for

spending, while too high a ratio would make small transactions

difficult and prevent the commodity from being sufficiently widely owned

in the prior barter economy. Gold still has these qualities today.

While fiat money has some of them, it fails the scarcity test: it is too

easy to create more of it.

The result of market competition is

not necessarily permanent. Market competition is an ongoing process.

Even when one commodity emerged as money, there continued to be

competition from other nonmonetary commodities. Once the world's money,

even gold could have lost its place had a superior alternative emerged.

But that is not the reason we no longer use it. Political money did not prove its

superiority through a market process. What happened instead was a

politically imposed change from a better system to a worse system.

Although

the central bankers have used political means to replace gold with

paper, they do not have the power to end the competition between their

money and commodity money. The "demonetization" of gold by central banks has rigged the competition—but not ended it.

Gold

as money may not be over for all time. As the monetary system melts

down, gold functions as "shadow money," an alternative that competes

with the political money. It remains a store of value because

of its potential to become money again. There is continuing demand for

gold as a hedge against the breakdown of the fiat system.

Governments

cannot force people to use their money beyond a point. The market will

only continue to accept fiat money as long as it works well enough (or

even, not too badly). If governments debase their currency beyond a

point where it maintains some value over time, people will stop using

government currency and switch to something else.

In countries

suffering hyperinflation (or even just excessive inflation), people

typically start quoting prices and accepting in trade in the more stable

currencies of other countries. Earlier this year, VietNamNet reported that land prices are being quoted in gold rather than the local currency, the dong.

The world is lurching through a serious monetary disorder. The proximate cause is the collapse of the housing bubble and the subprime-credit crisis, but the ultimate cause is the inherently unstable monetary system foisted upon us by a banking cartel. Central bankers are called upon to act as lenders of last resort, but in their efforts to inflate their way out of the credit collapse,

they risk igniting a hyperinflationary bonfire that will destroy the

world's major fiat currencies. Gold was money once, and could become so

again.

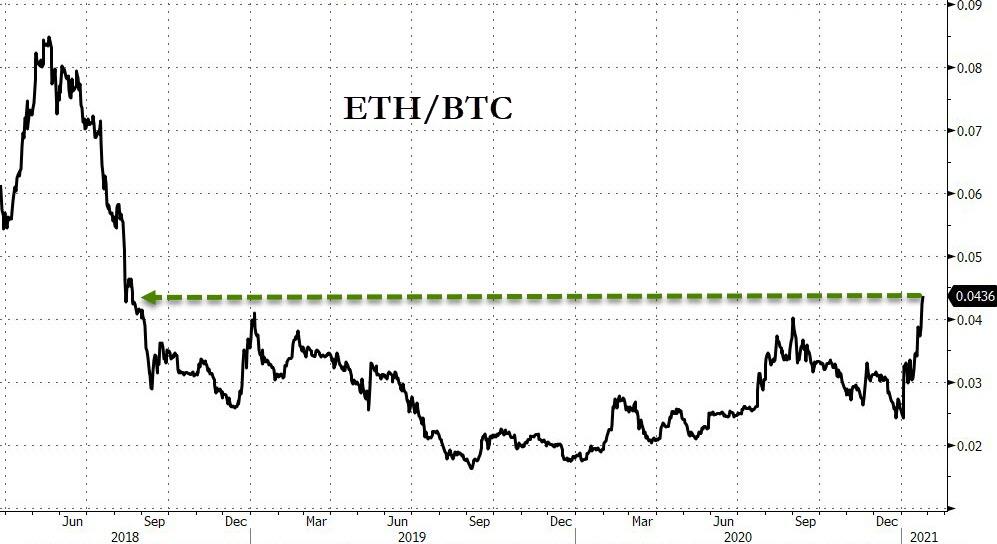

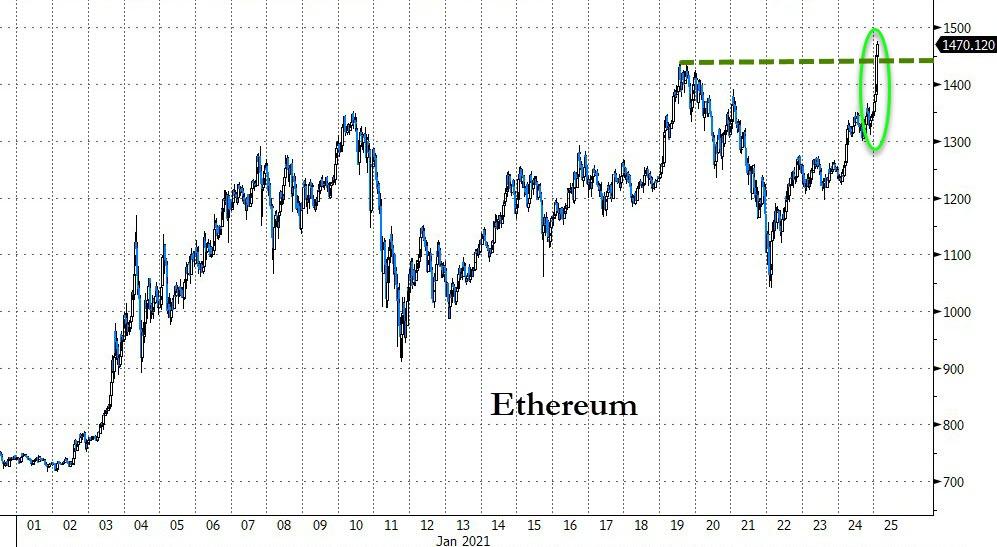

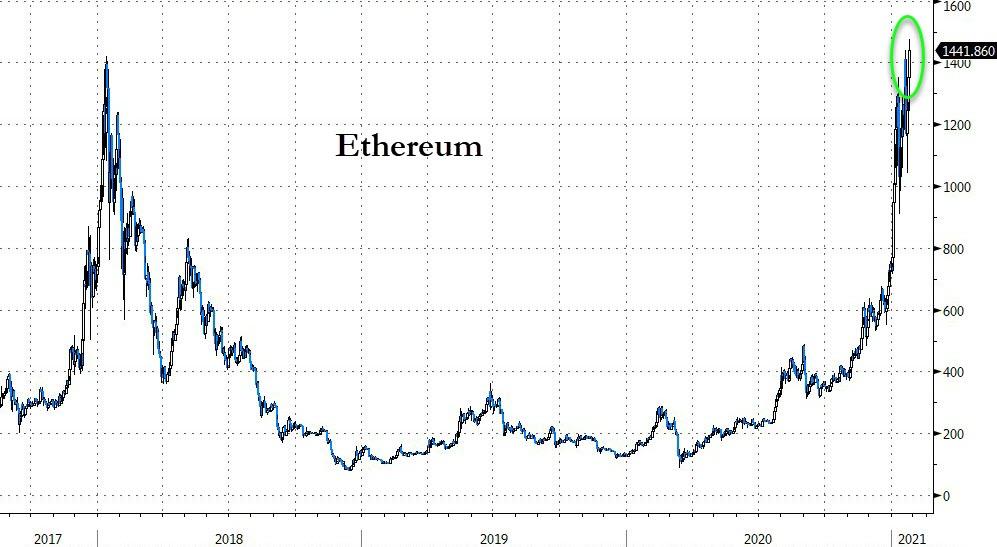

Coins that power decentralized finance (DeFi) protocols are soaring recently as bitcoin treads water.

While

bitcoin grabbed all the headlines early on in the year, it is the rest

of the crypto space that is stealing its thunder most recently as

Ethereum, the backbone of the smart contracts that define much of the

DeFi space, has drastically outperformed...

Source: Bloomberg

That is the highest for ETH relative to BTC since

Source: Bloomberg

In fact, as Bitcoin drifts, Ethereum is up over 17% since Friday...

Source: Bloomberg

Back above the recent highs....

Source: Bloomberg

Making new all-time highs...

Source: Bloomberg

The

incredible surge in the price of AAVE (driven as surge in the growth of

flash loans) most recently is a good example of what is driving this

push into DeFi tokens. As CoinTelegraph notes,

Flash loans allow cryptocurrency holders to collatoralize their portfolio to fund other purchases or new crypto purchases.

The loans also help investors utilize the value in their tokens without the need to sell see them and create a taxable event.

Since

launching flash loans less than 12 months ago, more than $1.7 billion

have been issued and it’s expected that this figure will increse as the

crypto bull market progresses.

Simply put, the crypto market is becoming its own bank.

Despite decrying censorship when it was happening to them last year, when Donald Trump was banned from Twitter and Facebook earlier this month, the left praised the move by big tech. “Facebook is a private company and can do what they want,”

the pro-censorship hypocritical crowd chanted ad nauseum through the

digital ether after bad orange man was silenced. But as we have said

time and again, Facebook being private is simply not true.

Now, however, Facebook

has made an unscrupulous Faustian bargain with the federal government

which should eliminate all doubt once and for all. They are now

willfully handing over private messages of Trump supporters who talked

about the events at the capitol on January 6.

Google, Apple, and Amazon all moved to wipe the pro-Trump social media network Parler from

the internet earlier this month because of what users on the platform

discussed. It was alleged that the handful of dolts who stormed the

capitol on January 6 had solely used Parler to plan their laughable,

unarmed, silly, unsuccessful, and pitiful attempt to keep Trump in the

White House.

Despite the ragtag group of Trumpians posing for selfies, photo-ops, and hanging from banisters, the only thing they accomplished was having D.C. turned into a scene akin to North Korea for Biden’s inauguration.

Most honest experts in the media have acknowledged that though a few

members of the mob thought they were part of some historic coup to keep

their leader in power, the idea that they had any real chance at an

insurrection was misleading at best and sheer propaganda used to further

the domestic police and surveillance state at worst.

Oh

gosh, I hope this doesn't mean the magnitude of the threat has been

wildly exaggerated for political gain, media excitement and ratings,

censorship orgies, and laying the foundation for a new fear-driven

Domestic War on Terror to control politics and information. https://t.co/oHhUPojpSO

Deferring all responsibility for the planning of the raid on the capitol, Facebook chief operating officer Sheryl Sandberg had stated shortly after the incident that the protests were largely organized off Facebook. However,

she was not telling the truth, and likely knew that large portions of

the pro-Trump protests were talked about and organized on Facebook. But

was Facebook wiped off the internet like Parler? No, no it was not.

Here’s why.

This week, Facebook began furnishing the

Federal Bureau of Investigation with data on Trump supporters who

discussed the events at the capitol on their platform - up to and including their private messages.Through this action the social media giant is acting as a de facto intelligence collecting arm of the US government.

In contrast, when Syed Farook, otherwise known as the San Bernardino mass shooter, wouldn’t unlock his iPhone for the feds, Apple

refused to create a backdoor for them to access it acting as an actual

private company supporting the privacy rights of its customers.

But Facebook is more than willing to open up its data mining services

for their friends in the federal government — because, as we have stated

numerous times, Facebook is not private.

As TFTP reported in 2018, Facebook announced that

it partnered with the arm of the government-funded Atlantic Council,

known as the Digital Forensic Research Lab that was brought on to help

the social media behemoth with “real-time insights and updates on

emerging threats and disinformation campaigns from around the world.”

The

Atlantic Council is the group that NATO uses to whitewash wars and

foster hatred toward Russia, which in turn allows them to continue to

justify themselves. It’s funded by arms manufacturers like Raytheon,

Lockheed Martin, and Boeing. It is also funded by billionaire oligarchs

like the Ukraine’s Victor Pinchuk and Saudi billionaire Bahaa Hariri.

The list goes on. The highly unethical HSBC group — who has been caught numerous times laundering money for cartels and terrorists —

is listed as one of their top donors. They are also funded by the

pharmaceutical industry, Google, Goldman Sachs and others. However, the

funding that comes from the United States, the US Army, and the Airforce

directly negates the “private” aspect of the partnership.

The

“think tank” Facebook partnered with to make decisions on who they

censor is directly funded by multiple state actors — including the

United States — which voids any and all claims that Facebook is a wholly

“private actor.”

The Atlantic Council wields massive

influence over mainstream media too, which is why when this partnership

was announced, no one in the mainstream press pointed it out as the

Orwellian idea that it is. Instead, headlines such as “US think tank’s tiny lab helps Facebook battle fake social media(Reuters)” and “Facebook partners with Atlantic Council to improve election security (The Hill)” were put out to spin the fact that a NATO propaganda arm is now censoring the information Americans see on Facebook.

But this partnership with the state-funded “think tank” is not the only reason Facebook is not private.

From government funded censorship arms to

the revolving door of high level bureaucrats who fill the ranks of the

oligopolies, the “private company” Facebook concept comes crashing down

when taking a closer look. Private-sector firms do not need to be

explicitly nationalized to further the establishment’s interests; it’s

enough to install their alumni in top regulatory positions. Through

these methods, Facebook can put on the façade of privatization while

actually acting as deputies for the state but alleviating any

constitutional checks in the process.

All the while,

whenever the censorship acts in their benefit, half of the masses cheer

it on and defend it, keeping resistance at a minimum.

What’s

more, as the government hangs the threat of antitrust litigation over

their heads, it can force these companies to act in their benefit even

without explicit partnerships like that of the Atlantic Council. In

fact, prior to the state getting involved in the talks of regulation

into big tech, information flowed relatively freely with Facebook only

removing racist and violent content. Now, however, as they bend to the

will of their partners in the federal government, people like myself

find ourselves on 30 day bans for saying “censorship leads to tyranny.”

This is why the answer to the government big tech censorship leviathan lies not in regulation but in boycott.

The time is now to get off these platforms who spy on you, ban you,

sell you to the highest bidder, and who are tearing society apart.

Censorship free platforms exist and are far more user friendly and treat

you as the actual customer instead of the sheep they are leading to

slaughter. You can check them out here.

Despite

the mandate of an education-loan policy to benefit poor students that

has been in place since 2001, India's public-sector banks continue to

deny student loans citing poor credit ratings.

INDRANIL MUKHERJEE/AFP/Getty Images

Nearly

twenty years after the National Democratic Alliance government

introduced an education loan scheme to benefit students from poor

families, India’s public banks continue to deny loans to students whose

parents have poor credit ratings. The Indian Banks’ Association, a

representative body of all banks with offices in the country, had

prepared this proposal as a model education loan scheme in 2000. The

next year, the NDA government announced the scheme in the union budget,

promising concessions to students wishing to pursue higher education,

and the Reserve Bank of India notified

it in April that year. But the experience of students and the

continuing need for judicial intervention indicates that the scheme’s

implementation is not steered by the benefit to aspiring students, but

by the caution of banks.

The RBI’s circular stated that the loan

scheme “aims at providing financial support from the banking system to

deserving/meritorious students for pursuing higher education in India

and abroad.” To be eligible under the scheme, students should have

scored 60 percent in the qualifying examinations for graduation courses;

for Scheduled Caste or Scheduled Tribe applicants, the requirement was

50 percent. The scheme permitted all commercial banks to provide loans

“subject to repaying capacity of parents/students,” with a ceiling of Rs

7.50 lakh for courses in India and Rs 15 lakh for courses abroad.

Further, it offered a moratorium on the repayment of the loan for the

period of the course and one year afterwards, or six months of getting a

job, whichever came earlier.

“The main emphasis is that every

meritorious student though poor is provided with an opportunity to

pursue education with the financial support from the banking system with

affordable terms and conditions,” the RBI’s circular stated. “No

deserving student is denied an opportunity to pursue higher education

for want of financial support.” Yet, students from economically

disadvantaged backgrounds who apply for an education loan are commonly

rejected by public-sector banks, citing their parents’ low CIBIL score. A

CIBIL score refers to a three-digit number issued by the Mumbai-based

credit-information company TransUnion CIBIL, which was formerly known as

the Credit Information Bureau India Limited.

Banks refer to this

score while assessing the creditworthiness of a potential borrower.

However, the RBI’s circular does indicate that the students, and not

their parents, are considered the principal borrowers. In fact, in

August 2015, the Indian Banks’ Association released “Revised Guidance

Notes” on the education loan scheme. “The student borrower has no credit

history and as such he is assumed to be creditworthy as this is a

futuristic loan,” the Guidance Notes state. It even addresses

circumstances where an applicant-student’s parents have a poor credit

rating. “It is likely that the joint borrower for the loan has a credit

history and any adverse features could have a bearing on the assessment

of credit risk … To overcome this, the bank may, as a prudent measure

insists on a joint borrower acceptable to the bank, in case of adverse

credit history of the parent/guardian of the student.”

But none of

these appear to be implemented in practice. Vani Rajeev, a student

pursuing her bachelor of science in radiology, was one such student

whose education-loan application was declined by the State Bank of India

citing her single mother’s poor credit history. “We had applied for the

loan in February,” Anju Jayan, Vani’s mother, told me on the phone. “My

daughter does not have her father. She only has me. I had a CIBIL

record since I had applied for a housing loan before. The loan was

rejected because of my CIBIL record.” In February 2020, Jayan applied

for a loan of Rs 4 lakh for her daughter’s education, but SBI’s

Kulasekharamangalam branch, in Kottayam, rejected the application soon

after.

In

July 2020, the Kerala High Court ruled in a similar case against a

decision by a branch of the same bank in Kerala’s Kollam district, where

a student’s loan application was rejected by the bank because of his

parents’ low CIBIL score. “I am of the opinion that unsatisfactory

credit scores of the parents of the petitioner cannot be a ground to

reject an educational loan in view of the fact that the repayment

capacity of the petitioner after his education should be the deciding

factor as per clause 10 of Ext R1 (a) scheme,” the verdict stated. The

exhibit cited by the court referred to a 2016 circular issued by the

IBA, which revised the original model education loan scheme to “enlarge

the coverage” and “address some of the weaknesses noticed.” The clause

10 mentioned in the judgment stated, “In the normal course, while

appraising the loan, the future income prospect of the student only will

be looked into.”

The petitioner in the case was a 20-year-old

student, Pranav SR, who had applied for an education loan of Rs 5,70,000

in order to pursue a bachelor of technology course in Tamil Nadu. The

loan application was rejected on the grounds that Shaji R, Pranav’s

father, had defaulted on a commercial vehicle loan, according to his

CIBIL report. “I paid the money that was due this month in the following

month,” Shaji explained to me. “I paid the dues this way for two

months. They informed me that my CIBIL score is low because I had a

month’s arrears pending.” Shaji then closed the vehicle loan so that

Pranav could apply again, but the bank rejected his application again

stating that his parents had poor credit histories.

Shaji said he

felt dismayed by the treatment of bank officials towards borrowers,

noting that his wife and Pranav had approached SBI’s Kadakkal branch to

apply for the loan. “The manager there told my wife that if you have

children, you should educate them only if you have money,” Shaji said.

“It really upset me to hear that. What is even more upsetting is that

they never bother to even accept the application by hand. They just ask

you to drop the application on the table and leave.” The application was

declined again, in May 2020.

The family

then moved the high court and received a favourable order in two months.

But even after the order, Shaji said, the bank tried to delay the

sanction of the loan “as much as possible,” before eventually processing

it. Their advocate, B Mohan Lal, said the bank officials were

“reluctant to comply” with the order. “We had to intimidate them with

the prospect of a contempt notice,” he said.

The

previous year, Lal had appeared for another student, Noorjahan NS, who

had filed a writ petition in the high court against SBI’s Kottarakara

branch in Kollam after her application for an education loan had been

rejected on similar grounds. Noorjahan had applied for a loan of Rs

7,40,000 to cover the expenses of her course at a dental college. As in

Pranav’s case, her loan was also rejected because of arrears on a

vehicle loan availed by her father. “I had bought a four-wheeler in 2010

on a long-term loan that could be repaid until 2017,” Najeeb Khan,

Noorjahan’s father, said. “I missed paying three instalments of the loan

on time. It affected my CIBIL score.”

The SBI’s counsel argued in

the case that the court cannot interfere “in a commercial decision of

the present nature.” However, the court observed that the loan scheme

was introduced as a “socially and economically relevant scheme” to

support the pursuit of higher education of students who may be in want

of financial assistance. The court finally ruled in Noorjahan’s favour,

noting that SBI’s rejection of the loan application based on her

parent’s credit score was arbitrary. The court stated that repayments

under this scheme “were contemplated to be made not on the financial

position of the parents but solely on the projected future earnings of

the students on employment after education.”

Lal pointed to the

similarities in the two cases. “In both the cases, the parties had paid

off their dues through a one-time settlement or otherwise,” he said.

“But when you apply for a loan and you have to deposit a particular

amount by say, 15th every month and you pay the amount on 16th, you are

treated as a defaulter. Even if you pay dues of two or five months in a

single instalment, you will still be a defaulting person. Then they will

always perceive you as a thief.”

The advocate also pointed out

that both students belong to Other Backward Classes, a fact mentioned in

both court orders. “In the case of Noorjahan, she had obtained

admission in the management quota in a self-financing college,” Lal told

me. A management quota refers to seats for admission that are filled by

a university based on its discretion, and not strictly by the general

eligibility criteria. “So they argued that she is not a meritorious

candidate. They raised the same point in the second case as well.” But

the IBA’s guidelines, as revised in 2015, stated that “a student getting

admission offer under merit quota may choose to take up a course under

management quota as a personal preference. Such students may be

sanctioned loans under this Model Scheme.”

Despite the recent

court orders, Lal said that rejection of education loans based on

parents’ CIBIL records continues to be commonplace, as reflected by the

case of Vani Rajeev. In July, soon after Pranav’s case was reported in

the papers, Rajeev approached SBI’s Kulasekharamangalam branch again,

and tried to argue her case using the high court’s ruling. “But they

said that they have received no such directive,” her mother Jayan told

me. She was working as an accountant in UAE until 2014, when she lost

her job and returned to Kerala. In desperation, Rajeev even wrote to the

prime minister Narendra Modi and the union finance minister Nirmala

Sitharaman, informing them of her situation, in October last year. “I am

requesting you with great agony and advice me to continue my studies to

support my family,” she wrote. “My only hope of survival is the

education loan.”

On

30 December, Rajeev received a letter from SBI referring to her letter

to the prime minister. It simply repeated that Jayan was denied the loan

because of her CIBIL score. The family was unsure about challenging the

bank’s decision in court because the legal fees would be expensive. “I

am educating her by borrowing money,” Jayan told me. “Denying her an

education is not an option.”

As early as 2011, the Madras High

Court had ruled that students are the principal borrowers of education

loans, and not their parents. In its judgment that year in the case of Hannah DotrisversusAssistant General Manager, State Bank of Mysore,

the court held, “The bank should adopt a more reasonable and pragmatic

approach to the entire issue bearing in mind that the repayment shall be

made by the student concerned, who avails loan and such repayment

commences after completion of her course of study.” Yet, public-sector

banks have continually denied the loans, leading the Madurai bench of

the Madras High Court to take note of it in 2018. Citing the 2011

judgment, the bench observed, “It is rather unfortunate that the

aforesaid order came to be passed in the year 2011 and various

subsequent orders of this court had also passed, even then the financial

institutions have been continuing to reject applications of this nature

on similar grounds.”

K Srinivasan, the convener of Education Loan

Task Force—a Chennai-based voluntary body that offers guidance to

students in the application process—said that housing and vehicle loans,

unlike education loans, are sanctioned after assessing the present

financial status of the borrower. “IBA has clarified that educational

loans have to be dealt with in an independent manner and not to be

linked to the CIBIL rating of your parents,” he said. In case a bank is

concerned about the credibility of a borrower because of their parent’s

poor CIBIL rating, Srinivasan suggested that a family member or anyone

who does not have a low CIBIL score can stand in as a third-party

guarantor on the repayment of the loan.

In 2015, the union

ministry of finance collaborated with the department of higher

education—under the ministry of human resources development—and the IBA

to launch Vidya Lakshmi, a web portal to ease the process of securing

education loans. According to Srinivasan, while the portal created a

single window for students to apply to multiple leading banks across the

country, its implementation has been poor. “You apply to three banks

but none of the banks will take it seriously and the students don’t know

where to complain. Nobody takes a decision because they think the other

person will,” he told me. He suggested that instead of a simultaneous

submission of loan requests to three banks, there should be a

hierarchical process where the student has to consult a second or a

third bank only after her first choice of bank declines her application.

Emailed

queries to the concerned SBI branches, the IBA and the MHRD went

unanswered. This piece will be updated if and when a response is

received.

Srinivasan pointed to one recurring factor that led to

mistrust between banks and borrowers in Tamil Nadu—during election

seasons in the state, political parties promise a waiver

on education loans. “It unnecessarily misguides the students,” he told

me, noting that he receives hundreds of queries from students who ask

him when the loan waiver would be implemented. “Later, when a statement

is given that it is not possible, no media will take it up. If DMK or

AIADMK declare that education loans will be written off, that will come

as a prominent news item. Then all students who borrowed will get

misled. With the hope that the government will write it off, they will

stop repayment.”

The data suggests a steady decline in education loans to less privileged students. In January 2020, the Business Standardreported

that according to RBI data, there has been a steady drop in the growth

of education loans since 2016, with outstanding loans contracting by 3.4

percent as of November 2019. The report further stated that high-value

loans—of above Rs 10 lakh—were rising, and only smaller loans, which

benefit the lesser privileged, were shrinking. According to RBI data,

the report stated, the sum of outstanding education loans smaller than

Rs 10 lakh declined from Rs 60,000 crore in March 2016 to Rs 53,000

crore by the end of November 2019. In December 2019, Sitharaman had said

that there is no proposal under consideration for waiver of education

loans, adding that banks have been instructed to adopt a “non-coercive

strategy” to recover the loans.

Srinivasan said education loans

were not a priority for the banks or for the government. “There are

serious attempts at every level—at the banks’ level, at the government

level—to discourage educational loans,” he said. “Nobody takes it

seriously. Interest subsidy also is not properly disbursed.” Srinivasan

added, “Education loan is an investment, it is not a loan at all. It is a

national investment, investment on the future knowledge of society.”

The IMA on Thursday announced a pan-India relay hunger strike of doctors starting

February 1, in protest against a notification issued by the Central

Council of Indian Medicine (CCIM) that authorises post-graduate

practitioners in specified streams of Ayurveda to perform general

surgical procedures, stating that it will lead to "mixopathy".

The Indian Medical Association (IMA)

is giving immediate directives to all members across the country to

launch the "Save Healthcare India Movement", the doctors' body said in a

statement.

Under the campaign, the IMA will launch a massive awareness drive

across the country as this is a clear threat to the safety of healthcare

of people.

Doctors will take turns to sit on the hunger strike 24x7

from February 1 and the IMA will release posters and banners to raise

awareness on the issue across the country, the statement said.

"All IMA members shall update their Members of Parliament and MLAs

regarding the true picture of the notification and the integration

policy. The IMA will also give its representations to all state

governments. Under this movement, all NGOs will be updated about the

core issues," it added.

Besides, all IMA members will write and convey their feelings to the prime minister, the association said.

Representatives of the IMA shall visit various places across the

country to raise awareness among the public and apprise various

associations from different countries of this "unscientific"

notification, it said, adding that the global voice of modern medicine

shall echo the feelings of the Indian Medical Association and its members.

The IMA has condemned the notification issued by the CCIM, a statutory

body under the AYUSH Ministry, authorising post-graduate practitioners

in specified streams of Ayurveda to be trained to perform surgical

procedures such as excisions of benign tumours, amputation of gangrene,

nasal and cataract operations.

The doctors' body further said the recent policy tilt, as evidenced in the medical pluralism advocated by the National Education

Policy 2020 and the four committees of NITI AAYOG for officially

integrating the systems of medicine in medical education, practice,

public health and administration as well as research ostensibly for a

"One Nation, One System" policy, will "ring the death knell of all

systems of medicine as a whole".

"The IMA respects all streams of healthcare. We object mixing of the

streams as it is unsafe and unscientific...one doctor cannot give all

systems of medicine to one patient. Mixing the Pathies and providing

substandard healthcare is definitely wrong.

"The IMA demands withdrawal of the CCIM order and dissolution of the

NITI AAYOG committees for integration. The IMA appeals to the government

to consider the sensitivity of the medical fraternity and take

appropriate steps. The IMA will be constrained to intensify the

agitation until the steps towards implementing mixopathy are abandoned,"

it said.